Key Outcomes

Explain why NMD assumptions (core stability, decay, repricing behaviour) dominate ALM results and planning outcomes.

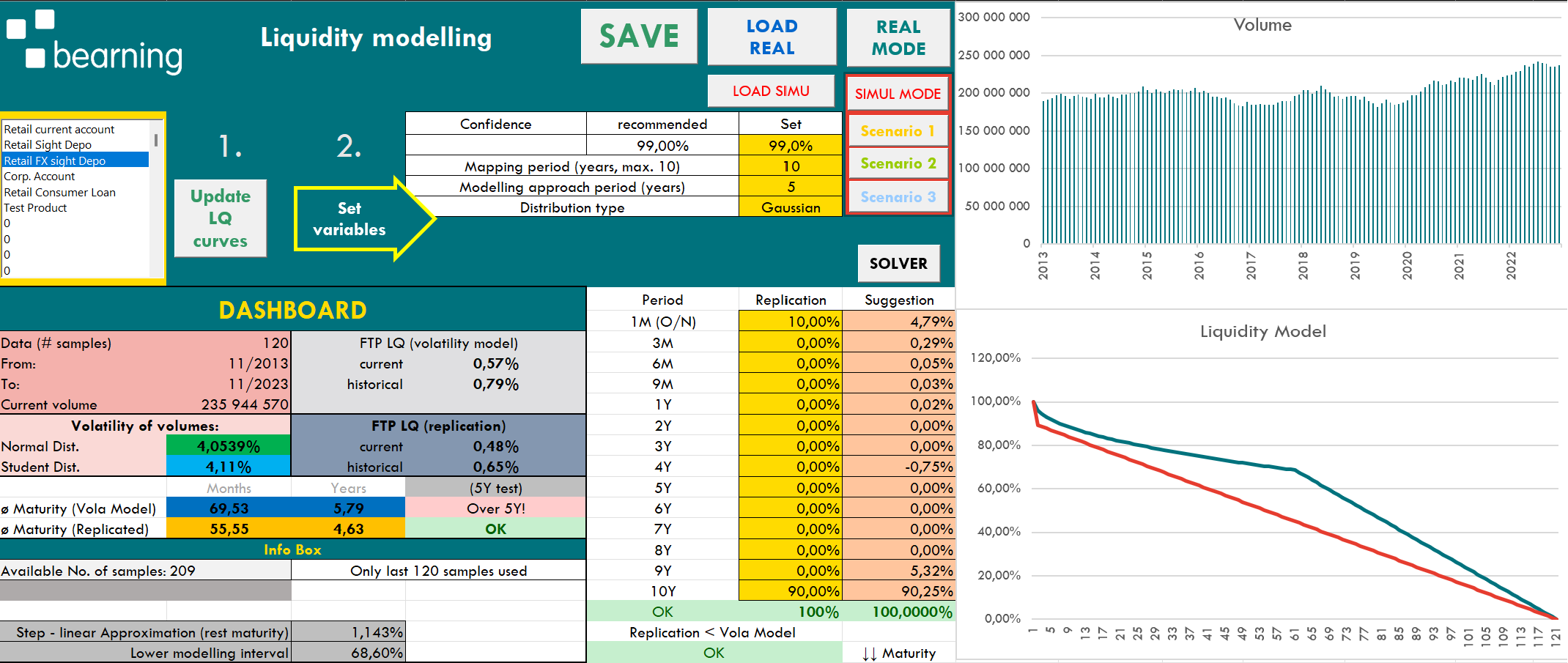

Build an NMD behavioural maturity profile (volume commitment) and translate it into a replication maturity distribution.

Build an NMD behavioural interest-rate profile (repricing/commitment) and translate it into an interest replication distribution aligned with the maturity profile.

Apply practical constraints and governance checks. Run scenario-based simulation for planning (volumes / rates / liquidity environment) and interpret impacts on IRR and margin dynamics.

Meet Our Speakers

Martin Macko

Bearning, CEO

Martin started his career in banking in 1994 as an MM&FX Treasury trader. Later he was appointed Treasury Director and Chairman of ALCO at a subsidiary of an international banking group. In 2007, Martin founded a consulting company. Later, Bearning expanded its activities to include professional banking education in the areas of ALM & Treasury, financial markets, risk management, fintech and digitalization. Martin holds several degrees and qualifications: Ing. (equivalent to M.Sc.) from the Slovak Technical University, ACI Dipl. (ACI Dipl.) from the Financial Markets Association, Financial Modeling & Valuation Analyst (FMVA)® and Certified Banking & Credit Analyst (CBCA)™ and Capital Markets & Securities Analyst (CMSA)® from the Corporate Finance Institute.

Michal Lopušan

QuantALM, founder

Michal graduated from Comenius University in 2005 with a degree in economics and financial mathematics. Since graduation he has worked for an international banking group in Central Europe as an ALM analyst. In 2009 Michal co-founded QuantALM - Quantitative Asset Liability Management team that developed the QuantPlan tool - a strategy and scenario based modelling system that banks can use to plan and manage their balance sheets. In addition, Michal broadened his education and is a CFA charterholder.

Non-Maturing Deposits (NMDs) Modelling for ALM & Planning

Join us on April 22nd from 14:00–17:00 CET (08:00–11:00 EST) for an in-depth session on Non-Maturing Deposits (NMDs) Modelling for ALM & Planning. Explore the behavioral modelling of NMDs and learn how to apply this knowledge in real-world scenarios to enhance your strategic planning. 14:00–14:10 – Introduction & Objectives Why it matters: NMD assumptions drive ALM risk and planning results. What we build: behavioral maturity + repricing profiles (replication portfolios). Practical output: Maturities set → liquidity premium + IR sensitivity set → product FTP assigned Validation on real-bank use cases with QuantPlan system. 14:10–14:35 – NMD modelling foundations (what we model and why) Core vs non-core intuition (stickiness = stable balances; volatility = balances that move/leave quickly) Separating two dimensions: (1) volume behavior (how long money stays); (2) repricing behavior (how customer rates react to market moves / higher funding costs) Model risks: maturities too long, repricing assumptions wrong, unstable results across samples, and weak performance under stress (outflows + faster repricing) 14:35–15:30 – Hands-on in Excel: Liquidity / Maturity modelling (Liquidity risk) Required inputs & data sanity checks (history length, granularity, outliers) Updating curves + interpreting historical volume behavior Choosing confidence interval, mapping/modelling horizon Building the maturity replication portfolio (with realism constraints) Reading and explaining results (summary + interpretation) 15:30–15:40 – ☕ Break (10 min) 15:40–16:00 – Hands-on in Excel: Interest-rate commitment / Repricing (IR risk) Data requirements: historical customer rates and the corresponding FTP/reference rates are needed to calibrate margin stability IR commitment: how behavioral repricing drives stable profitability (margin stability) Selecting an optimization approach to minimize margin volatility (practical comparisons) Building the interest rate replication portfolio Critical consistency check: IR profile must not exceed LQ profile maturity 16:00–17:00 – QuantPlan ALM Practical Lab: Real-bank NMD modelling Scenario simulation of an NMD product: comparison of three practical modelling views (attrition/run-off, average balance, core/non-core split) and step-by-step setup of a multi-factor approach in the planning tool. Planning view: scenario impacts on interest expense / margin and NII, incl. interest-rate moves, non-core outflows, and selected macro/micro drivers. Advanced use case: translating the multi-factor setup into clear planning inputs/outputs (Excel in/out) and interpreting the behavioral results consistently. Conclusion / governance: what to document — assumptions → calibration → outputs → planning interpretation (governance-ready). Final Takeaways and Q&A

Webinar Description

This advanced session takes you into one of the most sensitive ALM topics: behavioral modelling of non-maturing deposits (NMDs). You will learn how to define an NMD’s modelled maturity profile (liquidity behavior) and interest-rate risk profile (behavioral repricing / commitment) — the two building blocks needed for realistic balance sheet risk and planning. We first implement the full workflow hands-on in Bearning’s ALM_IRLQ Excel model, then validate the logic using real bank-style case studies and an implementation view in QuantPlan ALM. FTP for NMD products is a natural outcome of the modelling: once the replicated maturity profile and IR sensitivity are set, the corresponding liquidity premium and internal transfer rate based are easy to assign.

Ready to Master NMDs Modelling?

Unlock the secrets of NMDs modelling, enhance your ALM knowledge, and take your strategic planning to the next level. Join us on April 22nd!

€984,00